The $10K Challenge: DIY vs Institutional Risk | Adrian Rowles

The $10k Challenge: What Happened when a DIY Trader Went Head-to-Head with an Institutional Risk Framework?

A client looked me in the eye and said,

"Why would I pay you 2% percent when I can trade myself?"

I did not argue. I said fine, let's actually prove it.

We set up a real money challenge. His $10,000 USD account versus my $9,600 USD proprietary account. Same markets. Same timeframe. One year. No handicaps, no excuses waiting in the wings.

I want to be clear about something before I get into the numbers. I am not writing this to embarrass anyone. The client in question is smart, successful in his own industry, and genuinely confident in his own judgment. That confidence was exactly the problem. And I mean that in the nicest possible way, because I have seen it cost people far more than it cost him.

_____________________________________________________________________________________________________________________________________________________

The Setup

His side of this was simple. Full discretion. No restrictions, no rules, nobody second-guessing him at midnight when a position was moving the wrong way. Exactly the freedom most DIY investors say they want when they are explaining to me why they do not need an adviser.

My side was a separate Saxo proprietary account I funded personally with $9,600 USD. I used the same institutional risk framework I was trained in, working under former head traders at Goldman Sachs, the Managing Director of the Bank of America Options Trading Floor, and a Commerzbank hedge fund portfolio manager running multi-billion Euro long-short strategies. Not a backtest. Not theory. The actual framework they used with real capital.

Same ballpark capital. Same markets. One year.

_____________________________________________________________________________________________________________________________________________________

What Actually Happened

His account hit a margin call inside 90 days. Gone. He put in another $10,000 USD. By Q3, that was also gone. Second margin call.

Twenty thousand dollars. Less than twelve months. Zero advice fees paid.

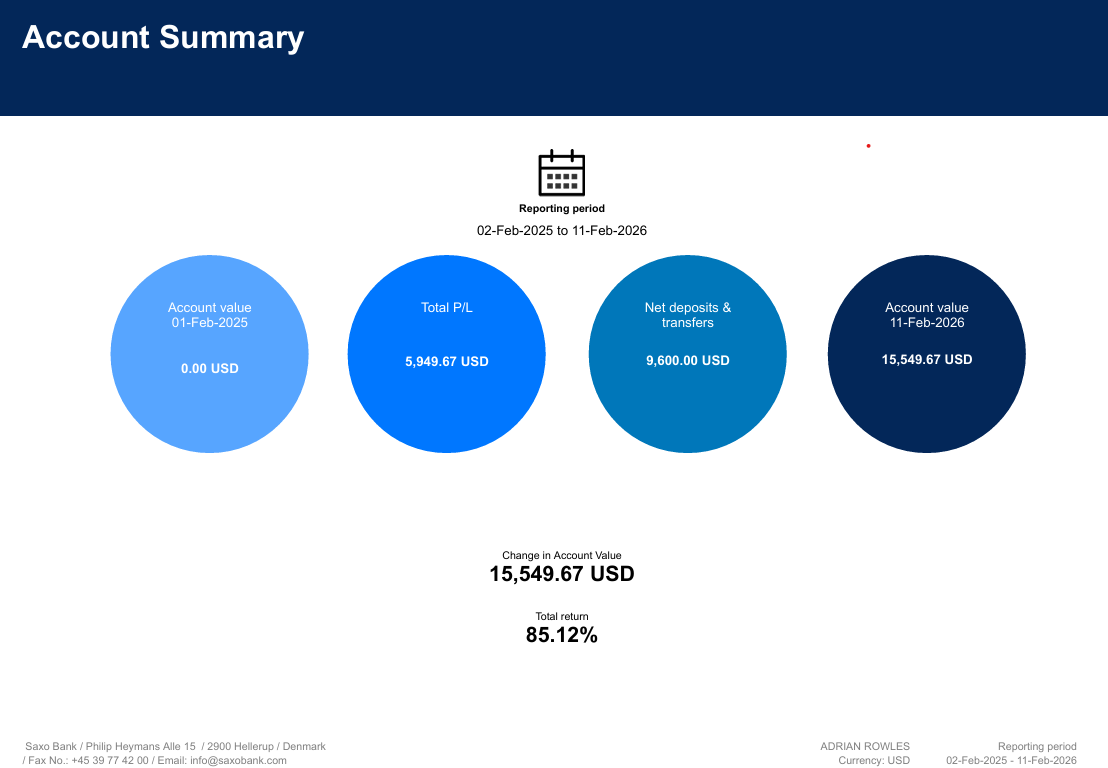

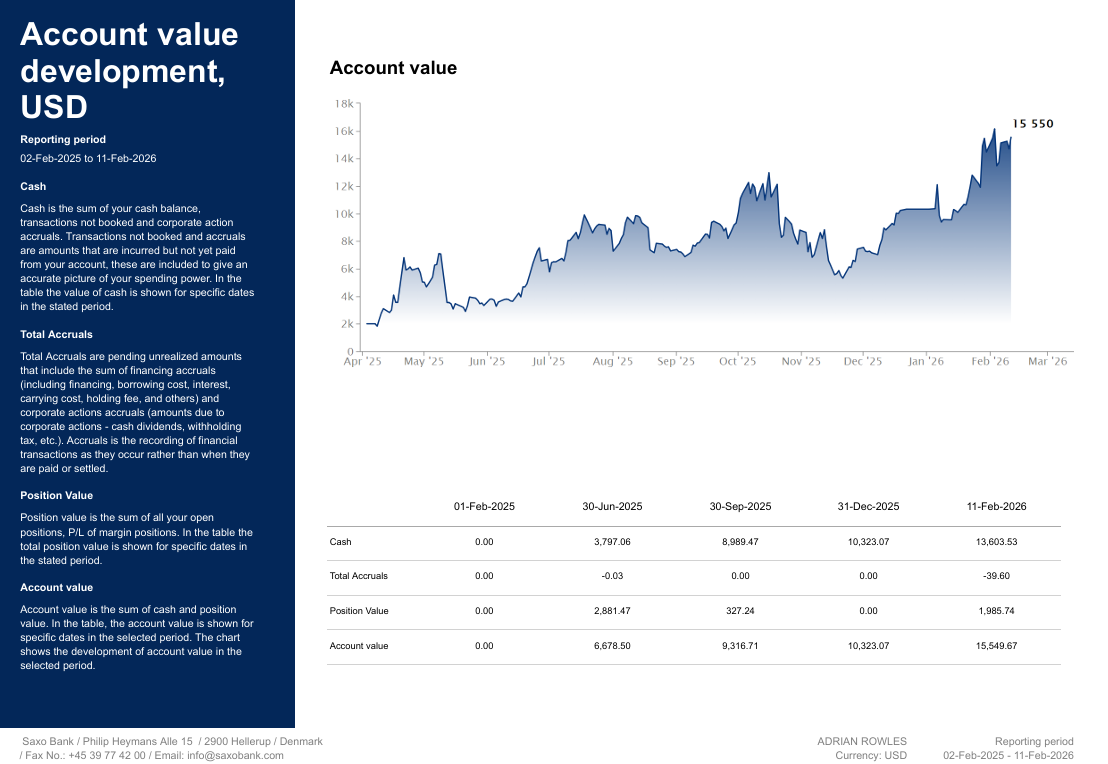

My account went from $9,600 USD to $15,549.67 USD over the same period. Roughly 85% percent net time-weighted return after all trading costs and financing.

Saxo account statement, $9,600 USD to $15,549.67 USD. 85% percent net time-weighted return. Full statement available on request.

Saxo account statement, $9,600 USD to $15,549.67 USD. 85% percent net time-weighted return. Full statement available on request._____________________________________________________________________________________________________________________________________________________

And yes, those costs were significant.

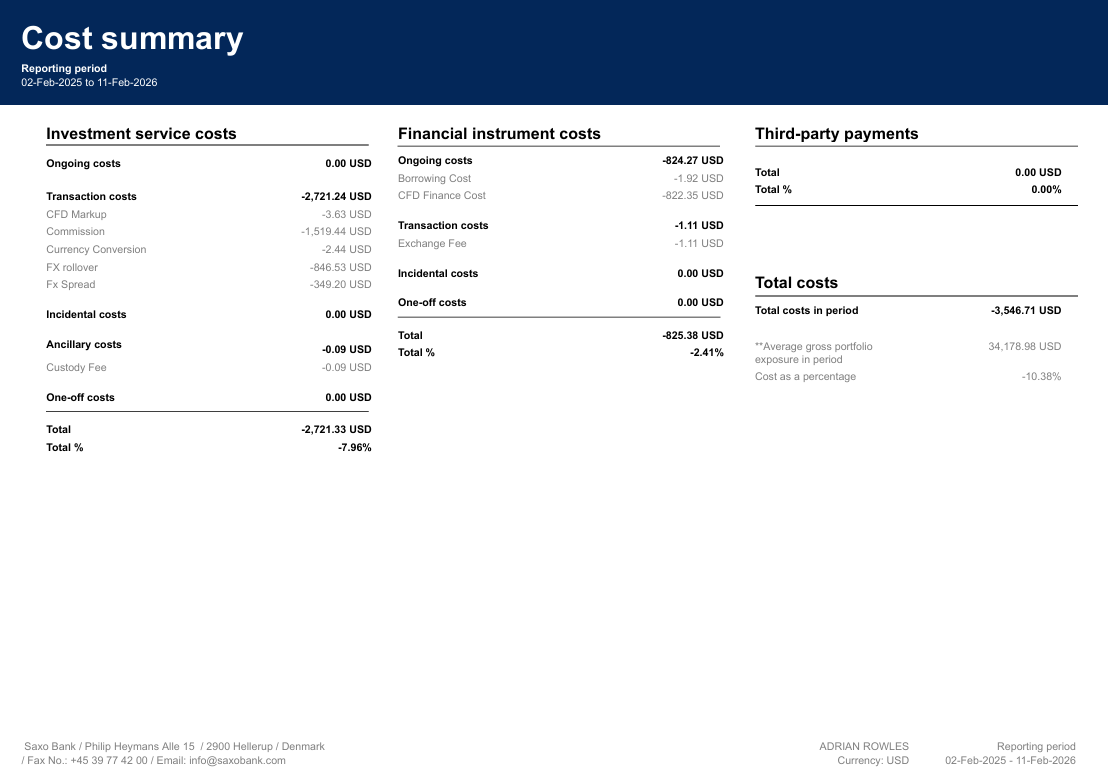

The account paid $3,546.71 USD in total trading friction, which works out to 36.9% percent of my initial deposit and about 10.38% percent of average gross exposure of $34,178.98 USD.

Total trading costs over the period: 3,546.71 USD, or 36.9% percent of initial deposit. More than 17 times what a 2 percent advice fee would have cost on 10,000 USD.

Total trading costs over the period: 3,546.71 USD, or 36.9% percent of initial deposit. More than 17 times what a 2 percent advice fee would have cost on 10,000 USD.

_____________________________________________________________________________________________________________________________________________________

So let me do the maths on the fee argument he made at the start. A 2 percent annual advice fee on 10,000 USD is about 200 dollars. He saved 200 dollars. Lost 20,000. I paid more than 17 times that 200 dollars in pure trading costs alone, and still grew the account by 85% percent net.

The most expensive advice is no advice at all.

I keep coming back to that line because I have not found a cleaner way to say it.

_____________________________________________________________________________________________________________________________________________________

The Part That Confuses Everyone

Most people, when they hear that, assume I must have been underwater by Christmas. The account grew by 85% percent. How?

It comes down to something that professional desks understand and retail traders almost never do. You do not need to be right most of the time. You need to make sure that when you are right, it pays more than when you are wrong. That asymmetry, across hundreds of trades, is where the actual edge lives. The win rate is almost a distraction.

Position sizing is the other piece. Every trade had a capped risk. Every theme had a capped risk. No single idea could blow the account up, regardless of how wrong I turned out to be. That is what kept the losing days from compounding into something unrecoverable. You survive first. Then you compound. That order matters enormously and it is the part most people skip.

I know this sounds counterintuitive. Social media finance content has spent years telling people they need a 70 or 80 percent win rate to come out ahead. That is just not how institutional desks think. They manage the full distribution of outcomes. A high hit rate is a vanity metric.

_____________________________________________________________________________________________________________________________________________________

The Fee Conversation Is Being Had Backwards

I read a lot of "how to choose a financial adviser" content. Almost all of it was written by people who have never actually managed risk in live markets. The advice is consistent: minimise fees, collect qualifications, be skeptical of active management.

None of that is wrong exactly. It is just catastrophically incomplete.

Fees matter. Obviously. But fees are one variable in a much bigger equation. You invest to end up with more money, net of everything, when it counts. Not to win a cost comparison contest with yourself.

The client in this story paid zero in advice fees. He also lost $20,000 dollars. A zero fee strategy that wipes out your capital is the most expensive strategy available. The maths on that is not subtle. The psychology of it is harder, because the fee is a visible, concrete number you can point at. The cost of bad risk management is invisible right up until it shows up as a margin call or a portfolio statement you do not want to open.

Fees have to be evaluated against the value of what you are actually getting and the risk of what happens without it. Not in isolation.

_____________________________________________________________________________________________________________________________________________________

"Fund Managers Can't Beat the Market" Is the Wrong Conversation

You have probably heard this one. Fund managers cannot beat the market, so why pay for active management at all? It is one of those lines that sounds very intelligent and misses the point almost entirely.

Most professional managers are not hired to beat the S&P every calendar year. Their actual mandate is usually something far more specific: deliver a target return that compounds over time, stay inside a defined risk budget, match a benchmark but with less drawdown pain along the way. The beauty contest against an index is something financial media invented. Most mandates do not actually care deeply about it.

Strong managers do beat their benchmarks. Consistently, over long cycles. But what they are really promising is risk-adjusted consistency you can actually live with for a decade. That is worth a lot more than most people give it credit for, and frankly a lot less than some managers claim.

Here is where I sit differently from most advisers: I work with fund managers and I am also a trained practitioner. That means when a product specialist gives me a polished pitch, I am not just nodding along and reading the factsheet back to clients later. I can ask hard questions about how they actually size positions, what drawdown controls look like in reality versus on paper, how costs eat into net returns at scale, and whether what I am looking at is genuine skill or a lucky three-year run in a benign market. Those are different conversations.

If your adviser has never managed risk in live markets, honestly, how equipped are they to answer those questions?

_____________________________________________________________________________________________________________________________________________________

Why the Training Background Actually Matters

People sometimes ask me this directly. "You trained with people from Goldman Sachs and Bank of America. But you are an adviser now. Are you not just picking funds like everyone else?"

Fair question. Short answer: no.

What that training gives me is the ability to act as a much more rigorous risk architect and gatekeeper on behalf of the people I work with. I can look at a manager's approach and have a genuine practitioner conversation about it, not a marketing conversation. I can tell the difference between an edge that holds up under scrutiny and one that looks good in a brochure. Most advisers cannot do that because they have never needed to.

My core work is mid to long-term planning. Pensions, cross-border structures, multi-asset portfolios for expats, high net worth individuals, business owners across the UAE, Japan and wider international markets. What is different is the lens I use. I think about those portfolios the way a trading desk thinks about a book. Risk budgets. Stress scenarios. Cost drag over time. The full range of possible outcomes, not just an average projected return on a slide.

_____________________________________________________________________________________________________________________________________________________

Questions Worth Asking Before You Sign Anything

Most "choose your adviser" articles are written to generate clicks, not to genuinely protect your capital. They will tell you to check qualifications, compare fees, and be wary of anyone claiming to beat the market. Fine, but not nearly enough.

If you have real money at stake, here is what I would want answered.

How do you manage risk over 10 to 20 years? Not in a model, not in a backtest, but in reality, when positions are moving against you, clients are calling, and the market is doing something nobody predicted.

How do you measure total cost drag? Not just the headline fee. The full picture: trading costs, product costs, financing, platform charges, and all of it quietly compounding against your wealth over decades.

Do you apply your framework to your own capital? Can you show me real performance through real drawdowns, not just a glossy prospectus?

Can you have a fluent conversation about win rate, payoff ratio, drawdowns and cost drag together? Or does everything come back to annualised return percentages?

If those questions get vague answers or a subject change, that tells you something.

_____________________________________________________________________________________________________________________________________________________

The Actual Punchline

I want to be careful not to oversell what this experiment proves. I am not claiming to be a great trader. I am claiming that a disciplined, institutional-grade risk framework applied consistently to real capital in real markets beat unstructured confidence. Every time I have seen these two things compete directly, it is not close.

This is not an invitation to copy trades. I do not sell signals or tips or any of that. I wrote this because the fee debate that dominates most advisory conversations is happening at the wrong level. People are optimising the wrong variable, and sometimes it costs them everything.

The framework behind this experiment is the same one I bring to every client relationship, whether that is an expat thinking about retirement, a business owner structuring long-term wealth, or a family office that wants someone who will genuinely push back on fund managers instead of amplifying their sales pitch.

The actual trading statement behind these numbers is available on request. If you want to sit down and talk through how this applies to your own situation, I am happy to do that.

Book a confidential call: calendly.com/adrianrowles

Email: adrian.rowles@acuma.ae

_____________________________________________________________________________________________________________________________________________________

Adrian Rowles is a financial adviser based in Dubai Marina, operating under AR Financial Advisor and Acuma. He serves individuals, businesses, corporates and family offices across the UAE, Japan and international markets, combining institutional-level training from former Goldman Sachs, Bank of America and Commerzbank hedge fund practitioners with AI-enhanced efficiency and advisory capabilities.