5 Surprising Truths About the AI Power Crisis: & Where the Smart Money Is Going

As the digital and physical worlds converge, will the next great tech titans look less like software companies and more like 21st-century power barons?

What is the status with power supply for the AI superscalars and Datacenters projects, where will it come from and what are the companies, governments and policymakers doing to address the gap, who is allocating capital and how much, what are the trade offs etc., how will local communities be positioned for power supply when the cash rich companies need a constant supply in a limited power resource world?

Introduction: The AI Boom's Dirty Little Secret

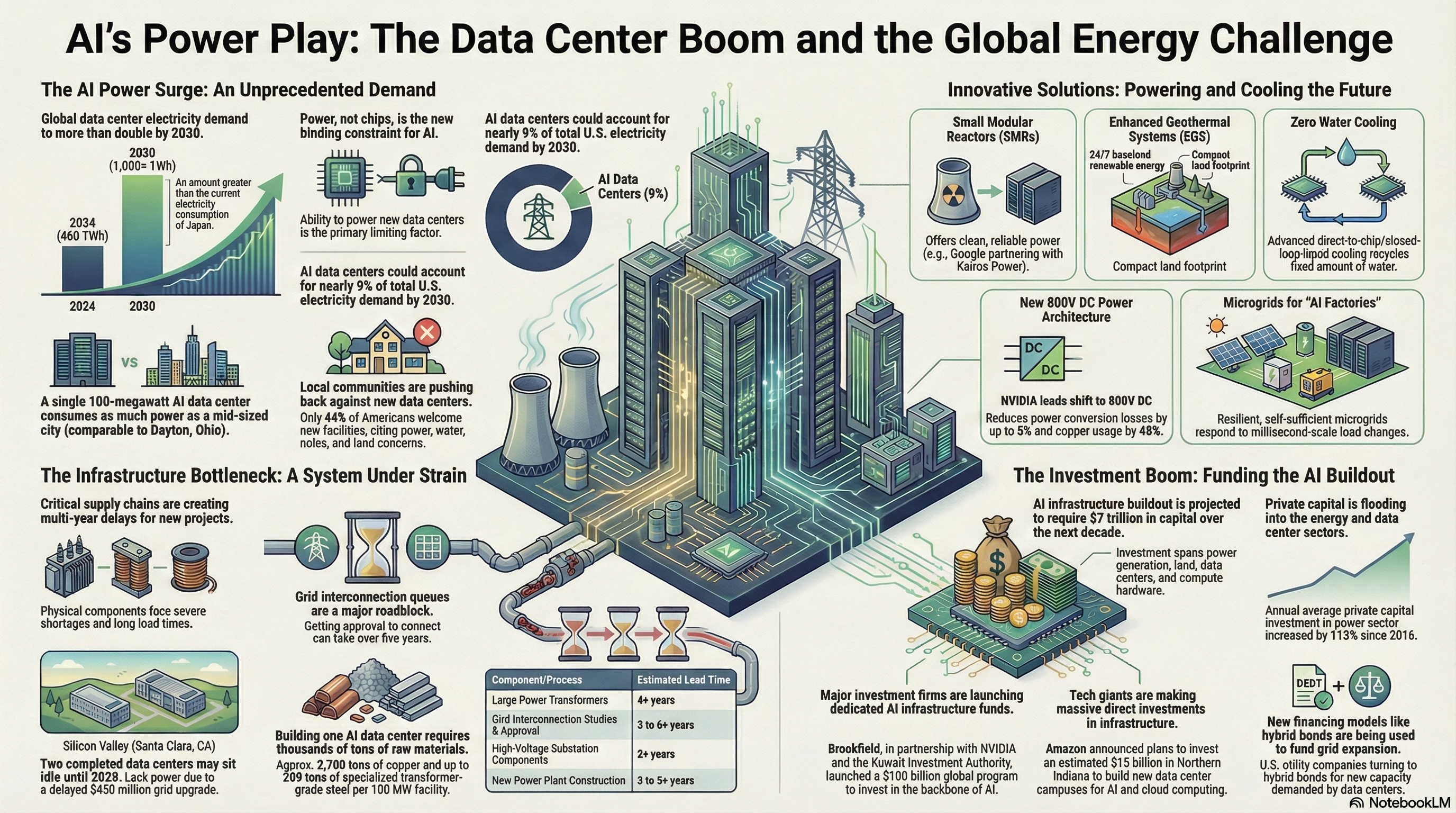

The artificial intelligence boom is in full force, and for the last two years, investor attention has been laser-focused on the semiconductor arms race. But as the world’s largest technology companies race to build out their AI capabilities, a less-discussed, more fundamental crisis is emerging: the monumental power shortage required to fuel this revolution. The reality is that for all the focus on advanced chips, power has become the "binding constraint" on AI's growth. This challenge, however, represents a generational investment opportunity for those who can look past the silicon and see the new architecture of power where true alpha will be generated.

--------------------------------------------------------------------------------

1. The Real Bottleneck: Why Power is the New Silicon

The primary constraint on the expansion of artificial intelligence is no longer the availability of semiconductor chips, but access to massive, reliable electrical power.

This demand shock is staggering in its scale. The International Energy Agency (IEA) projects that global electricity demand from data centers will more than double to 945 terawatt-hours (TWh) by 2030. Goldman Sachs forecasts a 165% increase in data center power demand by the end of the decade compared to 2023 levels. In the United States alone, McKinsey's analysis suggests data center demand could represent 30-40% of new net national electricity demand by 2030. This surge follows nearly two decades of flat electricity consumption in the U.S., creating what Douglas Jester, managing partner at the energy consulting firm 5 Lakes Energy, described as a "big shock" to the power system.

This fundamental shift was articulated by investor Steve Eisman: "there is a current binding constraint in AI and it's not chips... The binding constraint is power."

The strategic takeaway is unambiguous: the locus of critical infrastructure investment is shifting from the semiconductor fab to the substation. Capital allocation must follow this migration from compute manufacturing to power delivery.

--------------------------------------------------------------------------------

2. The Great Decoupling: Big Tech Is Becoming Big Energy

The inadequacy and congestion of the public electrical grid is forcing the world’s largest technology companies to become their own power producers, creating a new, vertically integrated asset class.

Grid interconnection delays now stretch for five or even ten years in some jurisdictions, a timeline that is completely untenable for AI’s rapid deployment schedule. A stark example comes from Santa Clara, California, where Digital Realty and a competitor have built massive data center facilities that are ready to go but have no power, potentially until 2028, due to grid upgrade delays.

This reality has forced hyperscalers to evolve into Independent Power Producers (IPPs), developing their own "behind-the-meter" (BTM) generation to bypass the grid entirely. This strategic pivot is transforming data centers from facilities defined by network latency into self-contained "AI Power Factories," where reliable power access is the core feature. This represents a powerful new form of vertical integration. In the same way that control over proprietary chips created a competitive advantage, control over proprietary power will now determine the speed and scale of AI deployment, creating a new class of infrastructure assets insulated from public grid vulnerabilities. This creates a new investment landscape focused on co-located power generation and integrated energy-digital campuses, where the value is in the power, not just the servers.

--------------------------------------------------------------------------------

3. The $100 Billion War Chests: Wall Street's All-In Bet on AI's Foundation

The world's largest private equity and infrastructure funds are deploying unprecedented amounts of capital to fund the transition to a power-first digital infrastructure, validating the scale of the opportunity.

This is not a niche or speculative play; it is a core, long-term thesis for the most sophisticated institutional investors. Consider the scale of recent commitments:

- Brookfield has launched a $100 billion global AI Infrastructure program to invest across the entire value chain, from energy and land to data centers.

- Blackstone recently closed its $5.6 billion Blackstone Energy Transition Partners IV fund, which specifically targets investments in grid reliability and power for data centers.

This flood of capital is essential. According to JLL, an estimated $170 billion in asset value will require development or permanent financing in 2025 alone. The massive war chests being assembled by Wall Street signal that the AI power problem is recognized as one of the most significant and durable infrastructure investment themes of the decade.

--------------------------------------------------------------------------------

4. From Sci-Fi to Balance Sheet: Nuclear and Geothermal Get Real

The unique demands of AI for 24/7, reliable, carbon-free baseload power are pushing once-niche energy sources into the commercial mainstream. To bypass a congested grid, these power sources must be sited directly next to data centers.

- Small Modular Reactors (SMRs): SMRs are emerging as a "preferred solution" because their continuous power production profile perfectly matches the constant demand of a data center. While commercial deployment in the U.S. is not expected until 2030 at the earliest, the technology is seen as a game-changer for AI data centers by enabling abundant, clean, and reliable on-site power.

- Enhanced Geothermal Systems (EGS): Geothermal offers a unique dual benefit. EGS taps into the Earth’s natural heat to provide steady, 24/7 electricity while also supporting direct-use cooling systems. This is a critical advantage, as cooling can account for up to 40% of a data center's total energy consumption. Recognizing this potential, the U.S. Department of Energy is actively funding demonstration projects like FORGE to accelerate the technology's deployment.

The investment implication is that the risk/return profile for these once-fringe technologies has been fundamentally altered. AI's non-negotiable demand for reliable, grid-independent power has transformed them from venture-style bets into core infrastructure necessities, creating a new, defensible asset class for long-term capital.

--------------------------------------------------------------------------------

5. The Social License: Why Water Is the New Carbon

A critical, and often overlooked, risk for data center investment is water consumption. This issue is driving both technological innovation and fierce local opposition that can derail projects entirely.

Data centers are incredibly thirsty. A large facility can consume up to 5 million gallons of water per day for cooling—equivalent to the water usage of a small town. This massive consumption of both water and energy is fueling bipartisan local opposition, or "NIMBYism," to new data center projects. This opposition is often rooted in complex local politics, where the trade-offs between environmental impact and economic benefit are stark. As one Oregon official noted, highlighting the debate over the quality versus quantity of jobs:

"The community doesn’t want to be overwhelmed with 10,000 jobs. Data centers with 200 jobs end up fitting in pretty nicely."

This social and regulatory pressure is forcing a technological shift toward water-neutral solutions. Microsoft, for instance, has launched a new data center design that consumes zero water for cooling by utilizing closed-loop liquid cooling systems that continually recycle water.

For investors, a data center's water strategy is now a critical factor in its long-term viability. This creates significant risk for projects in water-stressed regions using traditional cooling but presents a major opportunity for companies specializing in advanced, water-efficient liquid and immersion cooling technologies. For strategists, this means the cooling supply chain is no longer a component vendor market; it is a critical enabler of project bankability and a direct hedge against regulatory and social license risk.

--------------------------------------------------------------------------------

Conclusion: The Dawn of the Power-First Internet

The AI revolution is fundamentally an energy revolution. The old model of simply plugging massive server farms into a stable public grid is over. It is being replaced by a new paradigm of integrated, resilient, and localized power infrastructure where energy strategy dictates digital growth.

The investment thesis is now clear: power is the primary bottleneck, forcing hyperscalers into the energy business. Wall Street is funding this transition in force, and next-generation technologies like SMRs and water-neutral cooling are becoming prerequisites for deployment, not speculative options. As the digital and physical worlds converge, will the next great tech titans look less like software companies and more like 21st-century power barons?

--------------------------------------------------------------------------------

Author Bio

#AdrianRowles is a Dubai-based international financial advisor who has been privately trained and mentored by ITPM, former senior executives and proprietary traders from Goldman Sachs, Bank of America, J.P. Morgan and Commerzbank in institutional trading and portfolio management disciplines and processes designed to build consistently profitable portfolios, combined with advanced AI expertise, pioneering human and AI collaboration for expatriates, high net-worth individuals (HNWIs), family offices and corporates, delivering global market insights and institutional-grade strategies that support long term growth optimised with investor risk reward profiles.

If you would like to explore how AI infrastructure and resource-scarcity themes could be integrated into a diversified, risk-managed investment strategy tailored to your specific circumstances, goals and risk tolerance, you can book a complimentary 30-minute consultation at calendly.com/adrianrowles.