AI-Powered Strategies for Global Investors

The PC Memory Market Supercycle:

Why DRAM & NAND Prices Are Surging, and What It Means for Your Portfolio

Next-Gen Wealth Intelligence: AI-Powered Strategies for Global Investors

Edition: January 2026 | Adrian Rowles Financial Advisor Dubai

EXECUTIVE OVERVIEW: The Memory Crisis Reshaping Silicon

The PC memory market is in the grip of an unprecedented structural shift. DRAM prices have surged 171% year-over-year, while NAND flash contract prices have jumped 20–60% in a single month. This is not another cyclical glitch, this is a permanent reallocation of the world's silicon fabrication capacity, driven by artificial intelligence's insatiable appetite for memory.

Here is the scale: Global semiconductor revenues will exceed $1 trillion in 2026 for the first time in history, with memory and logic ICs driving growth of +30.7% year-over-year. But this is not broad-based prosperity. Memory sector growth of ~50% is concentrated entirely in AI infrastructure: high-bandwidth memory (HBM), server-grade DRAM, and enterprise SSDs. Meanwhile, commodity memory for PCs, smartphones, and consumer electronics faces scarcity and double-digit price inflation through at least late 2027.

The consequence: Hyperscalers and AI infrastructure players are thriving. PC makers and smartphone OEMs are facing margin compression. Investors who understand this shift can position portfolios to capture the winners and hedge against the losers.

SECTOR DYNAMICS: What's Happening in PC Memory Right Now?

The Core Problem: A Zero-Sum Supply Crunch

Memory chip manufacturers, Samsung, SK Hynix, and Micron, control ~95% of DRAM production and dominate NAND. They face an acute capacity constraint: fabricating high-bandwidth memory (HBM) for AI accelerators consumes 3x the wafer capacity per gigabyte compared to standard DRAM. Every wafer dedicated to HBM is a wafer denied to consumer products.

The result is a brutal prioritization hierarchy:

- Tier 1: HBM for AI (sold out through 2027)

- Server DRAM (DDR5) for data centre

- Enterprise SSDs for AI inference & training

- Tier 2: Legacy DRAM & NAND (rationed, rising prices)

- Consumer PC RAM (DDR4/DDR5)

- Mobile LPDDR memory for smartphones

- Client SSDs for laptops

- Tier 3: Commodity products (cut off, no allocation)

- Budget smartphone memory

- Legacy embedded systems

- Industrial & automotive applications

Price movements tell the story:

Product | Q4 2025 – Q1 2026 Price Change |

Server DRAM (HBM-adjacent) | +60% QoQ |

Conventional DRAM (DDR5 for PCs) | +55–60% QoQ |

Client SSD (laptop storage) | +40% QoQ |

NAND Flash (enterprise & client) | +33–38% QoQ |

Spot DRAM (commodity DDR4) | +100% month-on-month |

Why Manufacturers Are Hoarding Capacity

Memory makers are not expanding production; they are defending margins through supply discipline. Samsung, SK Hynix, and Micron have collectively announced $50+ billion in capital expenditure through 2026, but nearly all of it is directed at:

- HBM4 mass production (Samsung, SK Hynix both ramping in Feb 2026)

- Advanced process node transitions (1γ DRAM, hybrid bonding for chiplets)

- Yield improvements & equipment upgrades (not raw capacity expansion)

New production capacity will not materialize until late 2027 at earliest (Micron's Idaho facility, SK Hynix's Yongin M15X). Until then, pricing power remains with suppliers.

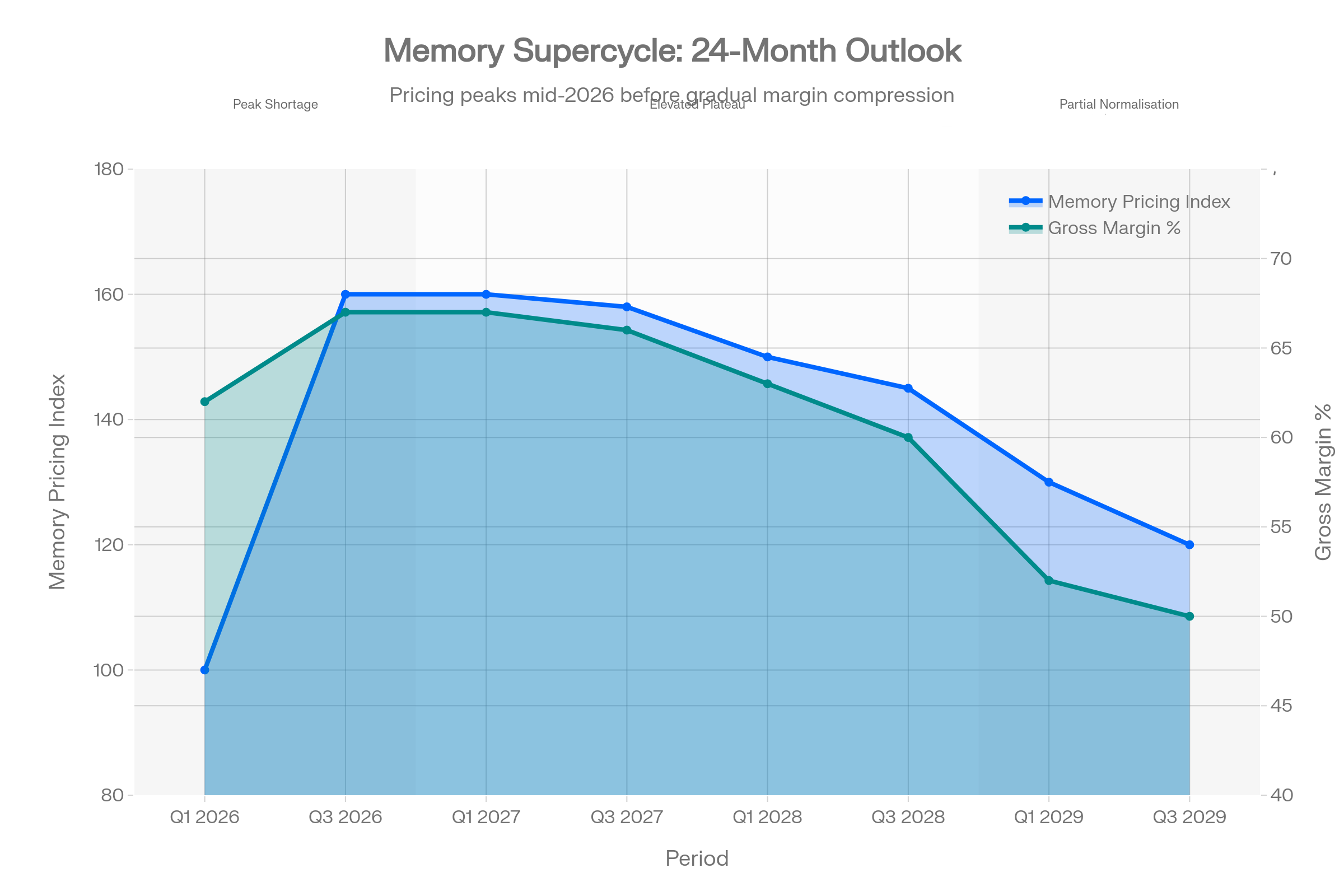

MARKET FORECASTS: How Long Will This Last?

Short-Term (Now – Q2 2026): Peak Shortage Phase

- DRAM prices: Further +40–50% increases expected by mid-2026.

- NAND prices: Stable to rising through Q2 2026

- PC DRAM shortages: Severe allocation constraints; lead times extending into mid-2026.

- Demand destruction: Budget PC and smartphone segments facing price resistance; expect 4–9% unit declines in 2026.

Medium-Term (H2 2026 – 2027): Pricing Plateau & Margin Peak

- Peak pricing likely mid-to-late 2026 (not early 2027 as some predict)

- Hyperscaler demand remains insatiable: OpenAI's Stargate project targets ~900 wafer starts/month by 2029 (vs ~450 current global monthly HBM output)

- Cloud pricing adjustments: AWS, Azure, Google Cloud likely pass through memory cost inflation to enterprise customers in 2026–2027 contracts.

- Consumer OEM pain: Dell, Lenovo, HP announce 15–20% PC price increases (already done as of Dec 2025); smaller brands face margin compression or exit.

Long-Term (2027–2029): Partial Normalization (Not Full Relief)

- New capacity arrives, but cautiously: Micron Idaho volume ramp mid-2027; SK Hynix Yongin by late 2027.

- Oversupply risk 2028–2029: If new capacity exceeds demand, pricing could revert to historical averages, but this is not the base case.

- Structural supercycle extends: Industry consensus (BofA, UBS, Citi) suggests elevated pricing persists through 2028, driven by:

- Continued AI infrastructure buildout (model training, inference scaling)

- Hyperscaler CapEx continuing at $500B+/year collectively.

- Automotive & industrial AI adoption ramping up (delayed by current PC shortage, resuming post-2027)

Consensus Forecast Summary (per TrendForce, IDC, SK Hynix investor guidance):

Supply tightness will persist until Q4 2027 at earliest. Memory prices will remain elevated through 2028. Partial relief only when new fabrication capacity achieves volume production in late 2027–2028.

SUPPLY CHAIN ARCHITECTURE & BOTTLENECKS

Geographic Concentration: A Single-Point-of-Failure Risk

Memory manufacturing is highly concentrated:

Metric | Reality |

DRAM market concentration | 95% controlled by 3 firms (Samsung, SK Hynix, Micron) |

DRAM fab locations | South Korea (60%), US (25%), Japan (15%) |

NAND market concentration | 90% controlled by top 5 firms |

Wafer fabrication complexity | Requires EUV lithography (ASML exclusive supplier) |

Equipment supply chain | Japan (Nikon, Canon), Netherlands (ASML), US (Applied Materials, KLA) |

Geopolitical risks:

- US export controls on HBM to China (implemented 2024, tightened Dec 2024): Blocks Chinese memory imports, forces CXMT (China's largest memory maker) to pursue indigenous HBM development (lagging by 3–5 years). Chinese retaliation: export license controls on rare earths, gallium, germanium.

- Taiwan semiconductor dependency: TSMC manufactures HBM chiplets for Samsung & SK Hynix via chiplet bonding models. Geopolitical crisis could cascade.

- Japanese equipment restrictions: US-Japan-Netherlands semiconductor coalition restricts EUV lithography exports to China; China weaponises rare earth export licenses in response.

Implication for investors: Diversification toward US-headquartered suppliers (Micron, Western Digital) and allied manufacturers (SK Hynix in South Korea, Samsung) offers geopolitical hedging.

Supply-Demand Imbalance: Structural, Not Cyclical

Demand drivers:

- AI training servers: 8–12 HBM modules per GPU (vs 2–4 per traditional processor)

- AI inference servers: 32–64GB DDR5 per node (vs 16GB legacy)

- Enterprise SSDs: 3–8TB per AI server (vs 0.5TB legacy)

- Total AI data-centre memory/storage per server: 4–6x consumer electronics

Supply response:

- New wafer capacity: ~0 bits added through 2026.

- Existing capacity reallocation: Manufacturers shifting 20–30% of DRAM fab capacity toward HBM.

- Yield improvements: EUV 1γ DRAM delivers ~30% more bits/wafer, but still insufficient to match AI demand growth.

Result: Demand growing 10–15% CAGR (AI buildout), while supply growing 5–8% CAGR (yield improvements + modest process node transitions). This gap persists until new fabs achieve volume: late 2027.

DISTRIBUTION & IMPORT/EXPORT CHALLENGES

Allocation Lockdown: Hyperscalers First

Major cloud service providers (CSPs), Microsoft, Amazon AWS, Google, Meta, are securing multi-quarter capacity commitments directly from manufacturers. This creates allocation scarcity for:

- PC OEMs (Dell, Lenovo, HP)

- Smartphone makers (Apple, Samsung, Xiaomi)

- Consumer retailers & module makers (Kingston, Corsair, TeamGroup, G.Skill)

Distribution impact:

- Lead times: Standard DRAM modules now 6–12 weeks out (vs 4–6 weeks pre-2024)

- Spot pricing volatility: Prices changing daily; offline quotes stale within hours.

- OEM bypass: Smaller PC makers forced to source through grey-market channels at 30–50% premiums.

- Module scarcity: 64GB DDR5 kits now $700+ (vs $120 in mid-2025); 256GB kits approaching $3,000.

Tariff & Geopolitical Pressures (2025–2026)

- US tariffs on imported electronics: 25% duty on semiconductors (proposed/implemented 2025); CSPs & OEMs accelerating nearshoring, increasing US manufacturing focus.

- CHIPS Act subsidies: Micron secured $6.165B in subsidies; priority US fab expansion (Idaho, Boise, Japan locations). Samsung & SK Hynix also expanding US presence.

- China supply chain bifurcation: US blocks HBM exports to China; China responds with rare earth export controls. Result: two competing semiconductor ecosystems emerging (US-allied vs China-allied)

INVESTMENT STRATEGIES:

Positioning for the Memory Supercycle

Theme 1:

Memory Oligopoly Upside (Winners: Samsung, SK Hynix, Micron)

Thesis: Elevated pricing + supply discipline = extraordinary profitability through 2027. Gross margins at 60–70% (vs historical 35–45%). Free cash flow surging.

Strategy:

- Allocate 40–50% of semiconductor exposure to memory plays.

- Weight toward SK Hynix (62% HBM market share, 70% HBM4 share for NVIDIA Rubin, sold out) and Micron (US-flagged, CHIPS Act beneficiary, margin upside)

- Samsung: More defensive; lower memory allocation (70% to consumer electronics hedges downside) but NAND + HBM upside

- Nanya Technology: Commodity DRAM play; lower margins but benefits from supply tightness (1.6% market share but with pricing power)

Time horizon: 12–18 months (hold through 2026 earnings cycle)

Risk factors:

- Trade war escalation reducing China demand.

- Demand destruction in consumer segments earlier than forecast!

- New capacity coming online faster than expected (low probability 2026, moderate 2027)

Theme 2:

Selective PC & Notebook Exposure (Winners: Premium Brands)

Thesis: Apple & Samsung have pricing power & supply agreements; budget OEMs face margin compression. Dell, HP, Lenovo passing through costs but losing volume.

Strategy:

- Reduce exposure to commodity PC makers (ASUS, Acer, MSI): margin compression unavoidable.

- Favour Apple & Samsung mobile: Can absorb cost inflation; loyal customer base accepts price increases.

- Consumer PC weakness expected through 2026: Expect 4–6% unit declines; revenue flat-to-down unless ASPs increase 10%+

- Enterprise segment more resilient: Corporates budget for 12–24-month refresh cycles; memory costs absorbed in CapEx, not passed to users.

Time horizon: 12–24 months (wait for cost stabilization)

Theme 3:

Enterprise SSD & Data Centre Storage (Winners: Kioxia, Samsung SSD division, Micron)

Thesis: Enterprise SSDs growing 35% CAGR through 2030 (vs 5–10% for client/consumer SSDs). AI data centres requiring 3–8TB per node; hyperscalers building out storage fabric.

Strategy:

- Allocate 15–20% of semiconductor portfolio to NAND flash (enterprise focus)

- Kioxia: Specialized in enterprise SSD; benefits from supply discipline (16.5% NAND share). More defensive than HBM plays, less cyclical.

- Samsung SSD division: Vertically integrated NAND + controller; margins expanding.

- Micron: Competing for enterprise SSD business; entering selective markets

Time horizon: 24–36 months (structural growth driver, less cyclical than HBM)

Theme 4:

Semiconductor Equipment & Chip Design (Defensive beneficiaries)

Thesis: Elevated memory pricing strengthens chipmaker profitability → higher CapEx for fabs → equipment vendors benefit.

Strategy:

- Applied Materials, KLA-Tencor, ASML: Benefit from memory CAPEX cycle (2026–2027)

- TSMC: GPU & logic chip demand remains robust; 28% of wafer capacity allocated to AI (vs 8% in 2020). Premium pricing sustained

- Memory IP providers: ARM, Cadence, Synopsys: License fees rise with memory CapEx

Time horizon: 12–24 months

COMPANY FUNDAMENTALS & CATALYSTS

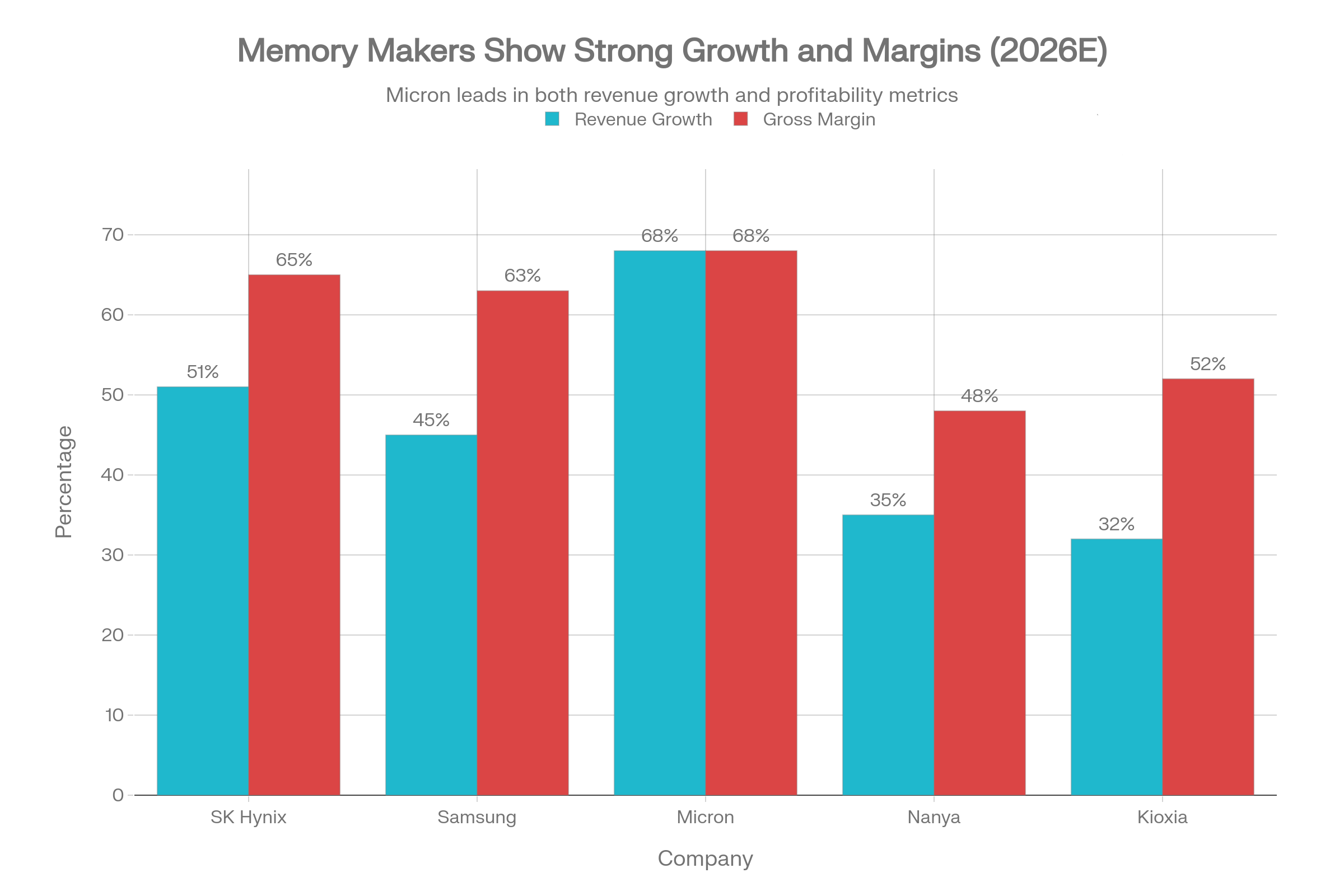

SK Hynix (000660.KS) – The HBM Kingpin

Business Model: DRAM (40% revenue), HBM (35%), NAND (25%)

Q3 2025 Performance:

- DRAM revenue $13.79B; 36% market share (reclaimed from Samsung due to HBM leadership)

- DRAM ASP (+60% QoQ growth); gross margins expanding to 65%+

- HBM3E sold out; HBM4 already allocated through 2026.

2026 Outlook:

- Revenue growth: +51% YoY (consensus BofA)

- Gross margin: 65%+ (highest in industry)

- HBM4 production: Mass production starting Feb 2026 (3 months ahead of Samsung)

- UBS target: 70% HBM4 market share for NVIDIA's Rubin platform (2026)

- Catalysts: HBM4 revenue ramp; potential 20–30% margin expansion from 2025 baseline

Valuation: Trading at forward P/E of 6–8x (historically 10–12x). Significant upside if the Supercycle extends.

Risk: Memory cycle downturn; China retaliation on exports

Samsung Electronics (SSNLF) – The Diversified Giant

Business Model: Memory (DRAM 34.8%, NAND 29.1% market share), consumer electronics (60% of revenue)

Q3-Q4 2025 Performance:

- Q4 guidance: $93B revenue, $20B operating profit (highest in 3 years)

- Reclaimed DRAM market share from SK Hynix due to larger capacity base

- HBM3E ramp underway; HBM4 mass production planned Feb 2026 (same timing as SK Hynix)

2026 Outlook:

- Revenue growth: +45% YoY (consensus) – lower than SK Hynix due to consumer electronics dilution

- Memory gross margin: 62–65% (second-best after SK Hynix)

- 50% HBM capacity surge planned for 2026.

- Catalysts: HBM4 share gain; NAND price recovery; Samsung Galaxy price increases (9–12% ASP growth)

Valuation: Cheaper than SK Hynix (P/E 4–6x forward) due to consumer electronics drag; offers better risk/reward for diversified exposure.

Risk: Consumer electronics weakness in 2026 (PC, smartphone volume declines)

Micron Technology (MU, NASDAQ) – The US Player

Business Model: DRAM (50%), NAND (35%), enterprise SSD (15%)

Q1 FY2026 Performance (announced Dec 2025):

- Revenue: $13.64B (+56% YoY) – beat consensus by $1B

- Gross margin: 56.8%; Q2 guidance 67–68% (extraordinary)

- Operating income: $6.14B (45% operating margin); $8.41B operating cash flow

- EPS: $4.78 (beat $3.96 estimate by 20%)

- Q2 FY2026 guidance: $18.7B revenue (+37% seq; +68% YoY), $8.42 EPS, 68% gross margin

2026 Outlook:

- Revenue growth: +68% YoY (highest among majors)

- Gross margin: 67–68% sustained through 2026 (industry-leading)

- HBM ramp: Capacity expansions underway in Singapore, Boise, Japan; HBM4 production starting Q4 2026 (3–6 months behind competitors)

- CHIPS Act benefit: $6.165B in subsidies finalized (only US memory maker with secured funding); new Idaho fab coming online mid-2027

- Catalysts:

- Q2 (March 2026) earnings likely another guidance raise

- HBM4 revenue ramp (Q4 2026 onwards)

- New fab capacity online (mid-2027)

Valuation: Forward P/E 8–10x (reasonable given growth). Insider selling noted but fundamentals strengthening.

Upside scenarios:

- Bull case ($400+): Memory Supercycle extends through 2027; Micron gains HBM share; CHIPS Act subsidies accelerate capacity.

- Base case ($350–380): Current trends continue through 2026 with strong earnings.

- Risk case ($250–280): Trade war escalates; AI demand moderates; memory prices peak earlier.

Risk: Execution risk on HBM4; geopolitical headwinds (China export controls); cycle peak timing

Kioxia (K3607.JP) – The NAND Specialist

Business Model: NAND Flash (100% focus); enterprise SSDs growing.

Market Position: 16.5% NAND market share; third largest NAND player

2026 Outlook:

- Revenue growth: +32% YoY (consensus) – lower than HBM-focused peers but steady

- Gross margin: 52% (compressed by commodity NAND pressure)

- Enterprise SSD growth: +35% CAGR through 2030 (structural tailwind)

- CapEx discipline: Limited NAND expansion; focus on process node upgrades.

Investment thesis: More defensive than HBM plays; benefits from enterprise SSD growth (less cyclical). Suitable for risk-averse investors seeking NAND exposure.

Risk: Commodity NAND pricing pressure; limited upside vs HBM-focused plays

SECTOR COMPARABLE ANALYSIS

See chart for detailed sector comparables (Samsung, SK Hynix, Micron, Nanya Technology, Kioxia) showing:

- 2026E revenue growth

- Gross margin targets

- Market share

- Key catalysts

SUMMARY: INVESTMENT FRAMEWORK FOR 2026

High-Conviction Themes:

- Memory oligopoly (60% of opportunity): Own SK Hynix or Micron for highest growth; Samsung for diversification hedge

- Time horizon: 12–18 months

- Risk/reward: +40–80% upside, -30–40% downside if cycle turns early.

- Enterprise SSD & data centre storage (20% of opportunity): Add Kioxia or Samsung SSD for structural CAGR growth.

- Time horizon: 24–36 months

- Risk/reward: Steady +15–20% CAGR, lower volatility.

- Avoid PC OEM commodity plays (20% risk mitigation): Reduce exposure to Dell, HP, Lenovo, ASUS

- Margin pressure through 2026; value destruction likely

Hedging & Risk Management:

- Tariff exposure: Position 50% in US-headquartered memory (Micron) for tariff insulation.

- Geopolitical bifurcation: Balance Korea exposure (SK Hynix, Samsung) with US exposure (Micron) for supply chain resilience

- Cycle peak risk: Exit 25–30% at price targets (mid-2026) to de-risk; re-entry on pullbacks (2027) if fundamentals remain strong.

CONCLUSION: A Decade-Long Supercycle?

The PC memory market is not in crisis; it is in structural realignment. AI infrastructure has displaced consumer electronics as the primary demand driver, and this shift will persist for at least 5–7 years as training and inference scale. Memory pricing will remain elevated through 2028, with partial normalization only when new fab capacity achieves volume production in late 2027 onwards.

For global investors, particularly HNWIs, expats, and family offices, this presents a rare inflection point: concentrated, high-margin growth in a capital-efficient sector, with clear beneficiaries (memory makers, enterprise SSD players) and clear losers (commodity PC makers, smartphone brands).

The question is not whether AI demand will cool, it will. The question is how much new capacity arrives when. And on that timing hinge portfolio returns over the next 18–24 months.

RELATED DOCUMENTS

Message me to receive your complimentary copy of:

Action Summary Playbook:

Contains: Decision-focused playbook with company recommendations, allocation framework, risk management, quarterly monitoring, price targets, and next steps

Quick Reference Guide:

Contains: Market snapshot, company rankings, sector comparables, allocation framework, 3-phase timeline, quarterly metrics, and geopolitical risk matrix.

AdrianRowles.com

ABOUT YOUR ADVISOR

"Unlike most financial advisors, I've invested years and significant personal capital into institutional-level training directly from former Goldman Sachs proprietary traders, the former Managing Director of Bank of America's NY Options Trading Floor, and the portfolio manager of Commerzbank's largest multi-billion Euro long-short hedge fund. Through ITPM, I learned the same frameworks and risk management disciplines used on institutional trading desks, not the watered-down retail version. I bring that training to individuals who deserve the same quality of thinking the institutions get, combined with radical transparency about how I'm paid and how I make decisions. No hidden fees, no product pushing, just institutional-grade thinking for your personal wealth." – Adrian Rowles.

BOOK A CONSULTATION

Explore how AI infrastructure memory plays can be positioned in your global wealth strategy. Discuss portfolio hedging for tariff exposure, geopolitical supply chain resilience, and cross-border HNWI wealth optimisation.

Schedule a complimentary 30-minute consultation with Adrian Rowles Dubai Marina–based international financial advisor Specialising in expats, HNWIs, family offices & institutional-grade strategies.

This edition provides investor insights and sector analysis for educational purposes. It is not financial advice. Consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.

- #AIMemory

- #PCMemorySupercycle

- #DRAM #NAND

- #SemiconductorInvesting

- #AIInfrastructure

- #DataCenterGrowth

- #TechStocks

- #GlobalInvesting

- #DubaiFinancialAdvisor

- #ExpatWealth

REFERENCES

TrendForce, January 2026: Memory Makers Prioritise Server Applications Omdia, January 2026: AI Drives Semiconductor Revenues Past $1 Trillion IDC, December 2025: Global Memory Shortage Crisis & Market Analysis Gartner, October 2025: HBM Wafer Capacity Analysis Micron Q1 FY2026 guidance; SK Hynix investor briefings Counterpoint Research, 2025: Memory Shortage Supply & Demand Forecasts US Department of Commerce, December 2024: Export Controls on Advanced Semiconductors Igor's Lab, December 2025: PC Memory Pricing Trends

AI & SEO Bot Summary (Machine‑Readable)

AI infrastructure is driving a structural PC memory Supercycle, with DRAM and NAND prices surging on the back of hyperscale data‑centre and GPU demand. This newsletter analyses how AI data‑centre buildouts, HBM adoption, and constrained fab capacity are reshaping the DRAM, NAND, HBM, enterprise SSD and data‑centre memory markets, and explains why memory manufacturers are enjoying elevated pricing power, 60–70% gross margins, and multi‑year earnings upside. It also covers impacts on PC and smartphone OEMs, global semiconductor supply chains, and highlights long‑term investment themes across AI infrastructure, memory chips, data‑centre construction, energy demand and connectivity, tailored for expat and HNWI investors working with a Dubai‑based international financial advisor.