Private Credit Risk 2026: What HNW Investors Holding BDCs and CLOs Need to Know Now

Here's what I'm seeing; and what I think you should actually do about it.

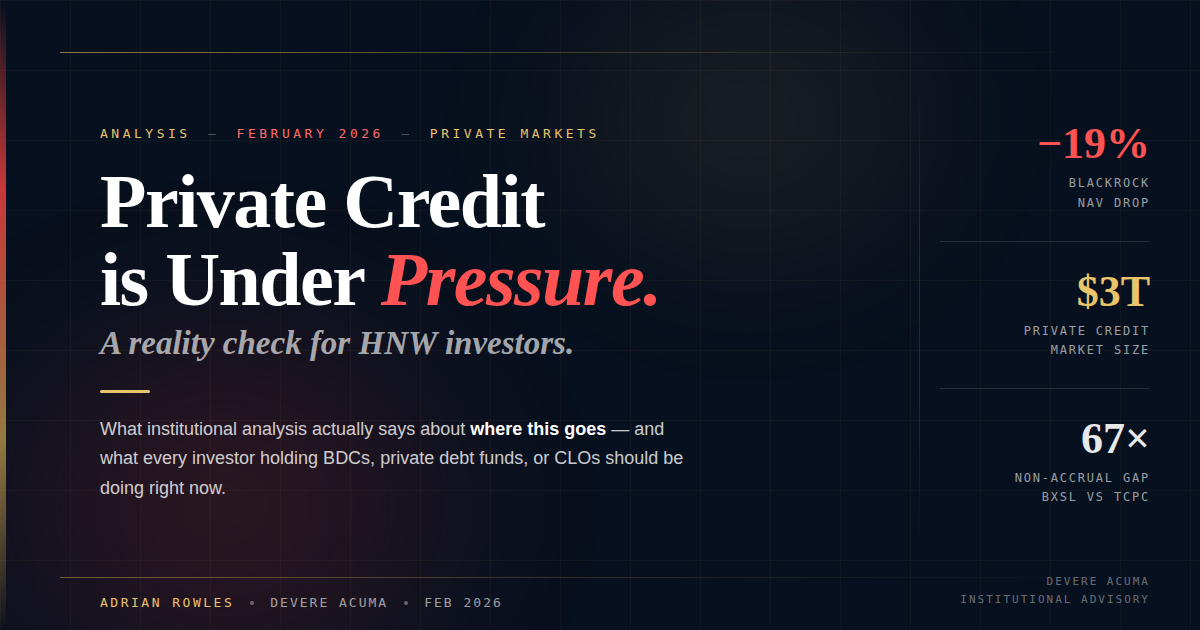

Adrian Rowles | dV Acuma | February 2026

So, January 2026. BlackRock marks down its private credit fund by nineteen percent. NAV goes from $8.71 to $7.05. Roughly a billion dollars, gone, formally acknowledged. And the reaction from most of the market was... muted. Not because people didn't notice, but because the people who track this stuff closely had been watching the warning signs stack up for a while and weren't particularly surprised.

Before I get into the numbers, I want to be upfront: I've been watching private credit more closely than usual for about 18 months. It started with something I kept noticing that well known fund managers, speaking across various media channels since late 2023 (and more frequently lately), making cautious and very specific observations about deal quality. Not alarm bells. Just the kind of careful, measured language that people who've lived through real credit cycles use when something is bothering them. My training under former Goldman Sachs and BoA NY prop desk traders, and a Europe hedge fund manager gave me the lens to read what they were actually saying between the lines.

This piece is for anyone who holds BDCs, private debt fund positions, CLOs, or any direct lending exposure. It's also for advisors who are trying to figure out how to have this conversation with clients before the statements arrive with bad news rather than after.

What this asset class actually is - and what got glossed over

Private credit went from roughly $500 billion to over $3 trillion in about a decade. A big chunk of that growth came from filling a void that banks left after 2008; middle market leveraged buyouts, PE rollups, companies bought at peak valuations that needed financing and couldn't get it from traditional lenders.

The investor pitch was simple: 8 to 12 percent yields versus 4 or 5 percent on investment-grade bonds, professional management, deal flow unavailable to public market investors. Sounds good. Mostly was good, for a while.

But there were structural things that didn't get enough airtime in the pitch. You can't exit quickly, this is fundamental and worth really sitting with, not just acknowledging and moving on. The underlying holdings are opaque. Most vehicles hold 70 to 100 companies and when credit stress materialises, those supposedly uncorrelated assets have a tendency to move down together. The illiquidity premium is real but so is the illiquidity, and the market conditions that compress those two things into an actual problem are not absent right now.

Most investors have exposure through BDCs that trade on exchanges like TCPC or ARCC, private debt funds with multi-year lockups, or CLOs where your real risk depends entirely on your position in the capital structure; AAA versus equity tranche is a completely different conversation.

The data, and why the headline number undersells the problem

Sources: Q4 2025 fund filings, Pitchbook private credit default tracker, Bloomberg credit data - cited throughout.

Headline default rate across the space is sitting around 1.45 percent. That's technically accurate and also genuinely misleading, it excludes restructurings and Payment-in-Kind arrangements, which is where a lot of the real stress is hiding.

PIK: Payment in Kind is when a borrower accrues interest instead of paying it in cash. The loan doesn't default. The fund records the income. The borrower's debt balance grows. It looks fine on the surface and it isn't. When you fold PIKs and restructurings into the default calculation, most analysts I've seen work through this get to something closer to 5 percent real impairment rate. That gap between 1.45 and 5 matters a lot depending on how concentrated your exposure is.

Here's the stat that I think tells the story most clearly. TCPC - a major BDC - has a non-accrual rate of around 20 percent as of Q4 2025 filings. BXSL has 0.3 percent. Same asset class. Same category label on your statement. Sixty-seven times different in terms of portfolio stress. If someone has both in a portfolio described as 'private credit exposure' those are not equivalent risks and shouldn't be treated as such.

Also worth knowing: roughly 92 percent of deals originated in 2021 and 2022 were covenant-lite, meaning lenders gave up most of their legal ability to force repayment if things deteriorated. Those deals are hitting refinancing walls now at rates much higher than the original terms. Some companies will manage it. Others won't, and the covenant protections that would have allowed early intervention mostly don't exist.

BDCs trading at 15 to 30 percent below stated NAV are doing something informative; the market is pricing in markdowns that haven't been formally announced yet. It's worth checking where each of your positions sits relative to stated NAV right now, not because the discount is automatic evidence of fraud or mismanagement, but because it's usually a leading indicator of what the next formal statement will say.

What I actually think happens from here

I'll be honest, I'm a bit allergic to the 'here are my scenario probabilities: 60% base case, 25% stress, 10% tail risk' format because the false precision bothers me. Nobody knows. Those numbers are a communication device, not analysis.

What I do think, directionally: the path through 2026 looks like continued deterioration in the weaker parts of the market. Default rates climbing into the 3 to 4 percent range in real terms. More BDC NAV markdowns coming some already flagged, more to announce. Dividend cuts at the lower-quality vehicles. If you're in good positions and sized correctly, it's an uncomfortable period that you can weather.

The scenario I'd push people to actually think hard about, not because it's the most likely outcome, but because it's the one that creates genuine problems if you're not positioned for it — is redemption gates. When investor outflows outpace the fund's ability to sell assets, funds suspend withdrawals. It happened in UK commercial property funds. It happened across hedge funds in 2008. The structural conditions for it in private credit are not hypothetical right now. If you have a large locked-up position AND you have any reason you might need liquidity in the next 12 to 18 months; any reason, a property purchase, a business event, a family situation that needs to be on your radar now rather than when you're trying to submit a redemption request.

The bull case; rates drop, distressed borrowers get refinancing room, the sector stabilises, is possible. I just don't think the current macro setup makes it the most likely near-term path. Could be wrong on the timing.

Three people. Three real potential situations.

Constructed examples.

First situation: $250,000 into TCPC in 2023. Yield at the time was 10.5 percent, so $26,000 a year in dividends, consistent, clean-looking income. Advisor presented it as stable. Q4 2025 brought a 19 percent NAV markdown. The position is now worth somewhere between $200,000 and $210,000 and generating maybe $8,000 to $10,000 a year. That's a $40,000 to $50,000 principal loss plus losing around $16,000 to $18,000 of annual income. For context, BXSL - same category, genuinely different quality - is up around 15 percent year to date through the same market stress. The right position existed. They were just in the wrong one.

Second situation: $3 million into a private fund in 2022, five-year lockup, targeting 10 percent. Statements looked fine through 2024. In 2025 the manager letters started changing more language about 'portfolio management' and 'working through restructurings,' less specific numbers. The 2026 annual statement is going to show roughly 8 percent NAV decline. They want to exit. They can't. The fund has gated redemptions.

Third: someone who in mid-2025 actually sat down and calculated that they were at 18 percent private credit across their portfolio. Moved $400,000 from TCPC and CCAP into BXSL. Trimmed TCPC from 4 percent of portfolio to 1 percent. Sold half a locked-up fund position at an 8 percent haircut deliberately, to get liquidity back, and redeployed into public credit. TCPC is down 30 percent in 2026 so far. BXSL is up 12 percent. Net of all of it they're about 4 to 5 percent better off than they'd have been, and more importantly they have options. That last part, having options is underrated in how people think about portfolio construction.

None of these are meant to be horror stories. Two of them are. One of them isn't. The difference was one review, done early.

The framework; what actually holds up in this environment

Private credit at 5 to 10 percent of total portfolio, maximum. Within that, quality tier only: BXSL, ARCC, OBDC. TCPC, CCAP, FSK belong in a separate risk category. If you hold them, size them accordingly, which for most portfolios probably means small or not at all.

Single BDC position: no more than 3 percent of total portfolio. Single private fund: no more than 3 to 5 percent. Never lock up more than 10 percent of total capital for five or more years, that rule sounds conservative until you need liquidity and discover you're gated.

For every million in private credit, hold at least $1.5 million in investment-grade or high-yield public credit you can actually sell in days not quarters. Treasuries or cash at 10 to 15 percent of portfolio. Five percent in genuinely liquid assets at all times, unconditionally.

On TCPC's current yield; it's sitting around 22 percent right now. I want to be direct about this: that's not an opportunity. A yield that high in a stressed credit environment is the market pricing in further NAV decline and dividend cuts, not rewarding investor courage. I'd treat any BDC yield above 15 percent in this environment as a warning sign until there's specific evidence to the contrary. High yield in stressed credit is often the last thing you see before the cut gets announced.

What not to do: hold distressed positions purely to maintain income run rate. Accept lockups beyond five years at this point in the cycle. Ignore non-accrual rate increases because the NAV hasn't formally dropped yet. Or have the same manager appearing across multiple vehicles in your portfolio without accounting for the correlated exposure, that's a risk that's invisible until it isn't.

Conversations that should be happening but often aren't

Most advisors aren't having these conversations proactively. Some because they don't have the framework for it, some because the answers are uncomfortable, some because client portfolios got allocated to the category label and nobody looked hard enough at the underlying quality.

What investors should be asking: What is the actual non-accrual rate on each of my BDC positions right now, and where does that sit relative to the sector average? What percentage of my private fund income is PIK rather than cash? How much of each fund's portfolio came from 2021 to 2022 vintage deals? If I submitted a redemption request for my locked-up position today, what would the secondary market actually pay, not stated NAV, what would it actually clear for? Have you stress-tested my portfolio against a scenario where default rates double from here?

What advisors should be asking clients: What percentage of your net worth is in private credit, including indirect holdings? If this fund gates for 12 months, what does that do to your actual liquidity position? Are you holding the same manager across multiple positions without realising it? When you invested, what was your real understanding of the downside, versus what you were told about the upside?

There's a broader question underneath all of this: are you positioned for a realistic base case, or are you positioned for the optimistic case while telling yourself it's moderate? Those require different portfolios and the honest answer is uncomfortable in a lot of client meetings right now.

Four things, do them in order;

First: actually audit your exposure. Pull statements from the last three months. List every private credit position by name, current value, percentage of total portfolio. Non-accrual rate for each BDC - findable in fund filings, takes about 20 minutes per position. Lockup end dates. Stated yield versus actual distributions you've received. Do this before anything else. Most people haven't done it in one place.

Second: score each position honestly. High risk: non-accruals above 4 percent, PIK above 8 percent of income, heavy 2021-2022 vintage concentration. Lower risk: non-accruals under 1.5 percent, PIK under 3 percent, vintages spread across years. For private funds you need to ask the manager directly in writing.

Third: rebalance with a specific plan, not a vague intention. If you're above 10 percent total private credit, reduce. If you're concentrated in lower-quality vehicles, rotate toward quality-tier BDCs. If you have large locked-up positions you want out of, get on the redemption calendar now - secondary market exists but at a cost, and better to take that cost on your terms than under pressure.

Fourth: build a monitoring process that you'll actually use. Quarterly minimum. Per position: new markdowns, rating changes, any language shifts in manager communications. Non-accrual rate crossing 2 percent is a trigger for action, not a flag for further watching. The advisors who built this discipline in 2025 are the ones with something to show clients right now.

Private credit isn't structurally broken. Parts of it are genuinely stressed, and the stress is doing what market stress always does, it's separating the vehicles that were carefully constructed from the ones that weren't. Quality managers with disciplined underwriting will get through this. The problem is that a lot of money went into the category, not into the quality, and those are different things with different outcomes.

The investors who'll look back on this period as navigable are the ones who audited honestly, moved toward quality before they had to, and kept enough liquidity to have actual options. The others are waiting for a clear signal.

January 2026 was a pretty clear signal. $1 billion. Officially acknowledged. Overnight.

If you want to work through your specific exposure - not a general conversation, your actual positions with your actual numbers, I'm offering a complimentary 90-minute session to do exactly that. Book here: calendly.com/adrianrowles. Confidential.

Adrian Rowles: Financial Advisor

Institutional Portfolio Strategy | dV Acuma | Dubai, UAE

Trained by former Goldman Sachs head traders, Bank of America options floor management, and a hedge fund portfolio manager who ran a multi-billion long-short multi-asset book across Europe. Working with HNW individuals, family offices, and corporates across the Gulf, Asia, and Europe.

Glossary:

- BDC: Business Development Company - Listed lender to mid-sized companies

- CLO: Collateralised Loan Obligation - Loan-backed structured credit product

- NAV: Net Asset Value - Net asset value of fund holdings

- PIK: Payment-in-Kind - Interest accrued, not paid in cash

- Non-Accrual - Loans no longer paying interest

- Cov-Lite: Covenant-Lite - Loans with reduced lender protections

- Redemption Gate - Fund withdrawal suspension

- Vintage Risk - Exposure to peak-cycle deals

- Discount to NAV - Market pricing below asset value

Private credit risk in 2026 is no longer theoretical. Rising BDC non-accrual rates, elevated PIK income levels, covenant-lite refinancing pressure, and widening discounts to NAV are measurable indicators investors must monitor closely. Understanding these structural factors is essential for protecting capital in direct lending, CLO exposure, and private debt fund allocations.

Adrian Rowles advises HNW clients across the UAE and Asia on private credit positioning exposure and institutional portfolio construction